Best Insurance Leads: The 5 Metrics That Actually Matter

Every article about "best insurance leads" reads the same: a list of companies, their features, and their prices. They don't answer the real question: what actually makes a lead "best," and why are agents still struggling to close sales even when buying from "top-rated" companies?

The truth is brutal: most agents buying "best insurance leads" are paying $500-2,500 per sale while thinking they're getting a good deal. The companies selling those leads are making 3-5x profit margins because they've optimized their business model, not yours.

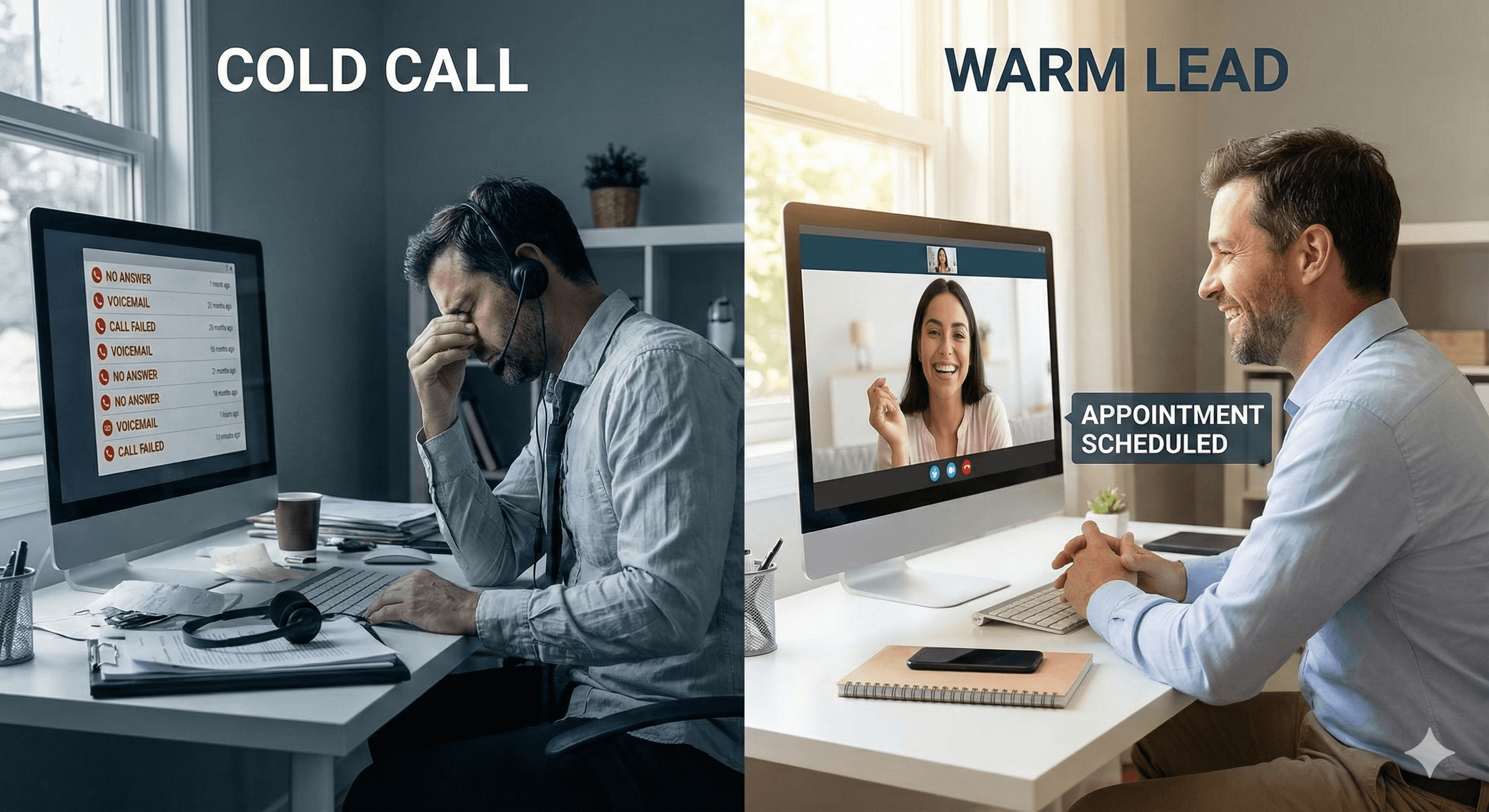

Best insurance leads are exclusive, warm, and self-qualified prospects who have already built trust with you before booking an appointment. They're not shared with competitors, they don't require cold calling, and they convert at 40-60% instead of 5-15%. Most "best" leads from companies fail all three criteria, which is why agents close 1-3 sales per 100 leads despite paying $2,500-5,000 monthly.

The difference between "best" leads and actual best leads is the relationship that exists before the first call.

The 5 Metrics That Actually Define "Best" Insurance Leads

Companies sell you on features: "real-time delivery," "exclusive access," "verified contact information." These are marketing tactics, not quality indicators. Here's what actually matters:

1. Exclusivity Score: How Many Agents Are Competing?

What Companies Tell You:

- "Exclusive leads available"

- "Limited distribution"

- "First-call advantage"

The Reality: Most companies sell each lead to 3-5 agents simultaneously. Even "exclusive" leads often have hidden distribution clauses or are sold to multiple agents in different regions.

How to Measure It: Ask the company: "How many agents receive this exact lead?" If the answer is anything other than "one," you're buying a shared lead. Shared leads mean you're competing with 4 other agents for the same prospect, reducing your close rate by 60-80%.

The Math:

- Shared lead (5 agents): 20% chance you're first to call, 5-10% close rate

- Exclusive lead (1 agent): 100% chance you're first, 8-15% close rate

- Branded lead (0 competitors): 100% chance you're first, 40-60% close rate

Best Practice: True exclusivity means the prospect requested an appointment with you specifically, not a generic quote request. This only happens with branded lead generation systems.

2. Warmth Index: Does the Prospect Know You Exist?

What Companies Tell You:

- "High-intent prospects"

- "Real-time delivery for immediate contact"

- "Qualified buyers"

The Reality: "High-intent" means they filled out a form. It doesn't mean they know you, trust you, or want to work with you specifically. You're still making a cold call to a stranger.

How to Measure It: Ask yourself: "Has this prospect seen my content, read my reviews, or heard my name before this call?" If the answer is no, it's a cold lead, regardless of how "fresh" or "exclusive" it is.

The Math:

- Cold lead (no relationship): 30-40% contact rate, 35-45% show rate, 5-15% close rate

- Warm lead (watched 5-10 videos): 60-70% contact rate, 70-80% show rate, 25-35% close rate

- Hot lead (watched 10-15 videos, requested appointment): 85-95% show rate, 40-60% close rate

Best Practice: The best insurance leads come from prospects who have consumed your content 10-15 times before booking. They're not cold—they're pre-sold.

3. Self-Qualification Rate: Did They Request You or a Quote?

What Companies Tell You:

- "Pre-qualified leads"

- "Budget-verified prospects"

- "Timeline-confirmed buyers"

The Reality: "Pre-qualified" usually means they answered demographic questions on a form. It doesn't mean they're ready to buy, have budget allocated, or want to work with you.

How to Measure It: The key question: "Did this prospect request an appointment with me, or did they request quotes from multiple agents?" If they requested quotes, they're shopping. If they requested you specifically, they're buying.

The Math:

- Quote request (shopping): 20-30% show rate, 5-10% close rate

- Appointment request (buying): 85-95% show rate, 40-60% close rate

Best Practice: The best insurance leads come from prospects who clicked "Book a Call" on your landing page after watching your content, not from filling out a generic comparison form.

4. True Cost Per Sale: The Number That Actually Matters

What Companies Tell You:

- "$15-50 per lead"

- "$75-150 for exclusive leads"

- "No contracts, cancel anytime"

The Reality: Cost per lead is a vanity metric. Cost per sale is what determines if you're profitable. Most agents buying "best" leads are paying $500-2,500 per sale without realizing it.

How to Calculate It: Track these metrics for 100 leads:

- Cost per lead: $25

- Contact rate: 35% (35 contacts)

- Show rate: 40% (14 appointments)

- Close rate: 10% (1.4 sales, round to 1-2)

True cost per sale:

- 100 leads × $25 = $2,500 investment

- 1-2 sales closed

- $1,250-2,500 per sale

Now add your time: 200 hours for 1-2 sales = $12.50-25 per hour effective rate.

Best Practice: The best insurance leads cost $50-150 per sale because they convert at 40-60% instead of 5-15%. This comes from branded systems, not lead companies.

5. Scalability Factor: Can You Grow Without Proportional Cost Increases?

What Companies Tell You:

- "Buy as many leads as you need"

- "Scale your business with our platform"

- "Unlimited lead access"

The Reality: Buying more leads means spending more money and more time. There's no compounding effect. You're renting, not building.

How to Measure It: Ask: "If I want to double my sales, do I need to double my lead spend and double my time?" With lead companies, the answer is yes. With branded systems, the answer is no—you increase ad spend, but your time investment stays the same because prospects self-qualify.

The Math:

- Lead buying: 200 leads = $5,000 + 400 hours = 2-4 sales

- Branded system: $5,000 ad spend = 15-30 sales with 5-10 hours of closing time

Best Practice: The best insurance leads come from systems that compound. Every month you run it, your database grows, your ad performance improves, and your cost per sale decreases.

Why "Best" Lead Companies Still Deliver Mediocre Results

The top-rated lead companies (EverQuote, QuoteWizard, InsuranceLeads.com, SmartFinancial, ZipQuote, Hometown Quotes) all have the same fundamental problem: they're selling shared leads or expensive "exclusive" leads that still require cold calling.

EverQuote: Market leader, $20-45 per lead, 30-40% contact rate, 5-10% close rate. True cost: $600-1,800 per sale.

QuoteWizard: Large network, $15-50 per lead, significant lead overlap reported. True cost: $500-2,000 per sale.

InsuranceLeads.com: High volume, $18-40 per lead, fast delivery but variable quality. True cost: $700-2,500 per sale.

SmartFinancial: Real-time delivery, $25-55 per lead, good speed but expensive. True cost: $800-2,200 per sale.

ZipQuote: Verified leads, $30-60 per lead, higher quality but limited volume. True cost: $600-1,500 per sale.

Hometown Quotes: Exclusive focus, $40-80 per lead, fewer duplicates but still cold. True cost: $1,200-3,000 per sale.

Notice the pattern: even the "best" companies result in true costs of $500-3,000 per sale. That's not a typo. That's the math of the shared lead model.

The Framework: How to Actually Get the Best Insurance Leads

If you're going to buy leads from companies (some agents do it while building their own system), use this framework to minimize damage:

Step 1: Calculate True Cost Per Sale, Not Cost Per Lead

Don't compare "$25 vs $35 per lead." Compare true cost per sale:

- Company A: $25 per lead, 8% close rate = $312.50 per sale

- Company B: $35 per lead, 12% close rate = $291.67 per sale

Company B is cheaper, even though the per-lead price is higher.

Step 2: Test Exclusivity Claims

Ask for proof: "Can you show me that this lead was only sold to me?" Most companies can't. If they can't prove exclusivity, assume it's shared.

Step 3: Track Contact Rate, Not Just Delivery Speed

"Real-time delivery" doesn't matter if the prospect doesn't answer. Track your contact rate. If it's below 40%, the leads aren't as "fresh" as advertised.

Step 4: Negotiate Return Policies Before Buying

Most companies offer returns, but the process is cumbersome. Negotiate clear terms: "If I can't contact this lead within 48 hours, I get a full credit, no questions asked." If they won't agree, they know the leads aren't that good.

Step 5: Use It as a Bridge, Not a Destination

Buying leads can work temporarily while you build your own system. But treating it as a permanent strategy means you'll always be renting, never owning.

The Alternative: Why Branded Lead Generation Creates the Actual Best Insurance Leads

The top 1% of insurance producers don't buy "best" leads from companies. They generate them using branded lead generation systems.

The Core Difference:

Lead companies: Cold prospects → Cold calls → 5-15% close rate → $500-2,500 per sale

Branded system: Prospects watch your content 10-15 times → Warm booking requests → 40-60% close rate → $50-150 per sale

How It Works:

Phase 1: Trust Building at Scale

You run short-form video ads (3-8 seconds) on Facebook, Instagram, and TikTok. These aren't sales pitches—they're micro-educational moments that position you as the expert.

Example: "Most people don't realize their term life insurance expires at age 65. If you're 45 and bought a 20-year term policy, you'll be uninsurable when it expires. Here's what to do instead..."

Prospects who watch 10-15 of these ads start recognizing your face, your voice, your expertise. When they see your booking page, they're not thinking "Who is this person?" They're thinking "I've seen this agent before. They know what they're talking about."

Phase 2: The Conversion Funnel

Your video ads drive to a dedicated landing page with a high-value offer:

- "Get Your Free Life Insurance Policy Audit: See if You're Overpaying or Underinsured"

- "Download: The 5 Questions Every 40+ Year Old Should Ask Before Buying Life Insurance"

The page includes social proof, addresses objections, and has a single, clear call-to-action: "Book Your Free Consultation."

Phase 3: Automated Nurture Sequence

Once a prospect enters your system, automation delivers:

- The promised content

- Educational emails

- Pre-framed sales conversations

- Urgency without pushiness

This sequence runs 24/7. You're not manually following up.

Phase 4: The Warm Appointment

By the time a prospect books a call, they've:

- Watched 10-15 of your videos

- Consumed your educational content

- Received multiple touchpoints

- Self-qualified by taking action

You're not making a cold call. You're having a consultation with someone who already trusts you.

The Results:

- Show rate: 85-95% (vs. 35-45% for cold leads)

- Close rate: 40-60% (vs. 5-15% for cold leads)

- Cost per sale: $50-150 (vs. $833-2,500 for cold leads)

The Math That Changes Everything

Let's compare the two models side-by-side:

Buying "Best" Leads from Companies (100 leads/month):

- Cost: $2,500/month

- Sales: 1-3/month

- Cost per sale: $833-2,500

- Time investment: 200 hours/month

- Scalability: Limited (more leads = more time)

Branded Lead Generation (Optimized System):

- Cost: $3,000-5,000/month (ad spend + service/education)

- Sales: 15-30/month

- Cost per sale: $100-200

- Time investment: 5-10 hours/month (mostly closing)

- Scalability: Unlimited (increase ad spend = more leads)

The branded system costs more upfront but delivers 10x the ROI. More importantly, it's an asset. Every month you run it, you're building a database of warm prospects, improving your ad performance, and creating a predictable revenue stream.

Buying leads is a recurring expense with diminishing returns. Branded lead generation is a capital investment that compounds.

What Most Agents Get Wrong About "Best" Insurance Leads

Mistake #1: Believing Price Equals Quality

$75-150 per "exclusive" lead sounds premium, but if it still requires cold calling and converts at 8-15%, it's not actually better. The best insurance leads aren't the most expensive—they're the ones that convert.

Mistake #2: Focusing on Delivery Speed Instead of Relationship

"Real-time delivery" doesn't matter if the prospect doesn't know you. A lead delivered in 5 minutes to a stranger is worse than a lead delivered in 24 hours to someone who's watched your content 10 times.

Mistake #3: Not Tracking True Costs

Cost per lead is a vanity metric. Cost per sale is what matters. Track contact rates, show rates, close rates, and time investment. The numbers will shock you.

Mistake #4: Treating It as a Long-Term Strategy

Buying leads can work as a temporary bridge while you build your own system. But treating it as a permanent strategy means you'll always be renting, never owning. You're building someone else's asset, not yours.

Mistake #5: Ignoring the Alternative

Most agents don't know branded lead generation exists. They assume buying from companies is the only option. Once you see the math, the alternative becomes obvious.

The Bottom Line: Best Insurance Leads Can't Be Bought—They Must Be Built

Insurance lead companies aren't evil. They're running profitable business models. The problem is those models don't serve agents long-term.

The agents making $200K+ per year aren't buying more "best" leads than everyone else. They're running better systems. They're building assets instead of paying for commodities.

If you're going to buy leads from companies, do it with your eyes open. Understand the true costs. Track your metrics. Use it as a bridge, not a destination.

But if you want to build something that compounds, invest in branded lead generation. Learn the system yourself or use a done-for-you service. Either way, you'll own the asset instead of renting the commodity.

The question isn't whether you can afford to build a branded lead system. It's whether you can afford not to.

If you're ready to stop buying "best" leads and start generating actual best leads, get our free ad scripts to see how the system works. Or explore our done-for-you service if you want results without the learning curve.

The old model is broken. The new model is here. The only question is: when are you going to make the switch?